How to avoid capital gains tax on real estate

Learn how to avoid capital gains tax on real estate with strategies like the primary residence exclusion, 1031 exchanges, basis boosts, and loss harve

Written by

Domain Money, CFP®

Capital gains tax is simply the IRS’s cut of your profit when you sell property. The good news for you is that with the right strategies, you can often reduce or even defer what you owe. Your best move depends on whether the property is your home, an investment, or part of a bigger financial plan. Here are some key takeaways to guide your decision-making:

Selling your property can feel like a win until you start thinking about capital gains tax. The good news is that you have a few options. With the right strategies, you can often reduce what you owe or even avoid taxes altogether, all while staying within the rules.

One of the most common tools is the primary residence exclusion. If you’ve lived in your home for at least two of the last five years, you may be able to exclude up to $250,000 in gains if you’re single, or $500,000 if you’re married and filing jointly. That’s a major difference when you’re ready to cash out on years of equity growth.

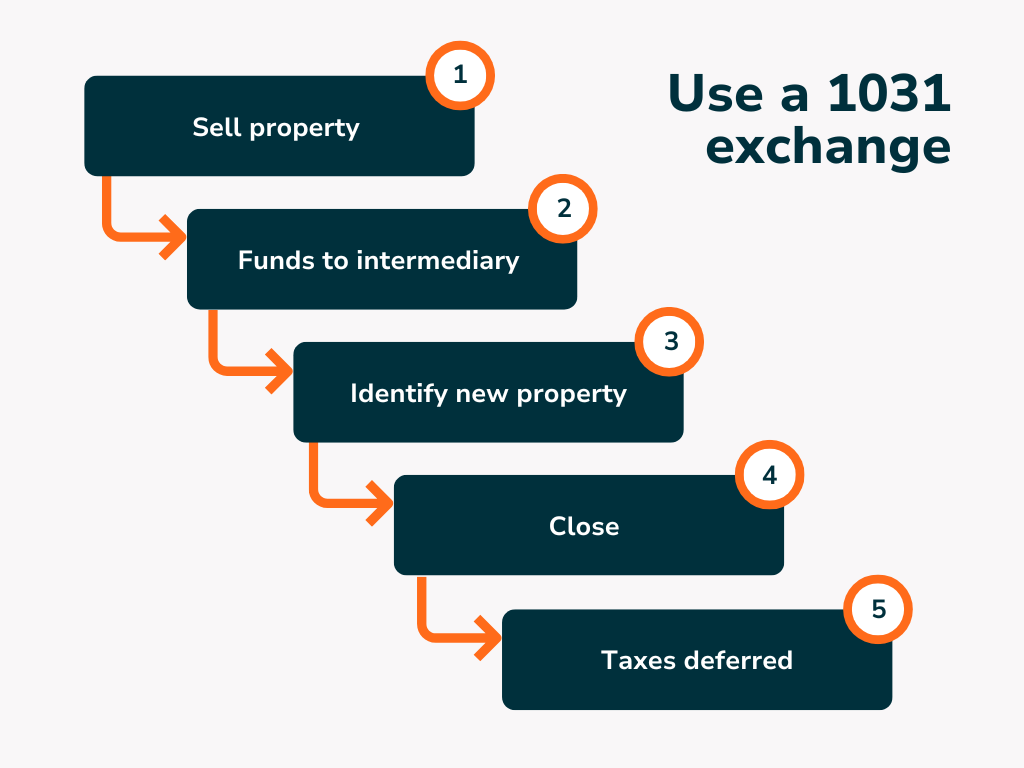

If you’re an investor, another powerful option is the 1031 exchange. This strategy lets you defer capital gains taxes by rolling your profits into another “like-kind” property.

These approaches can reshape the financial outcome of your sale. The key is knowing which strategy fits your situation, and often, that means getting guidance before you make a move.

When you sell real estate for more than you bought it, the profit is called a capital gain—and the IRS wants its share. That tax, known as capital gains tax, can shrink your earnings if you’re not prepared.

Here’s the simple breakdown:

Think of it like this: the longer you’ve held onto the property, the friendlier the tax treatment.

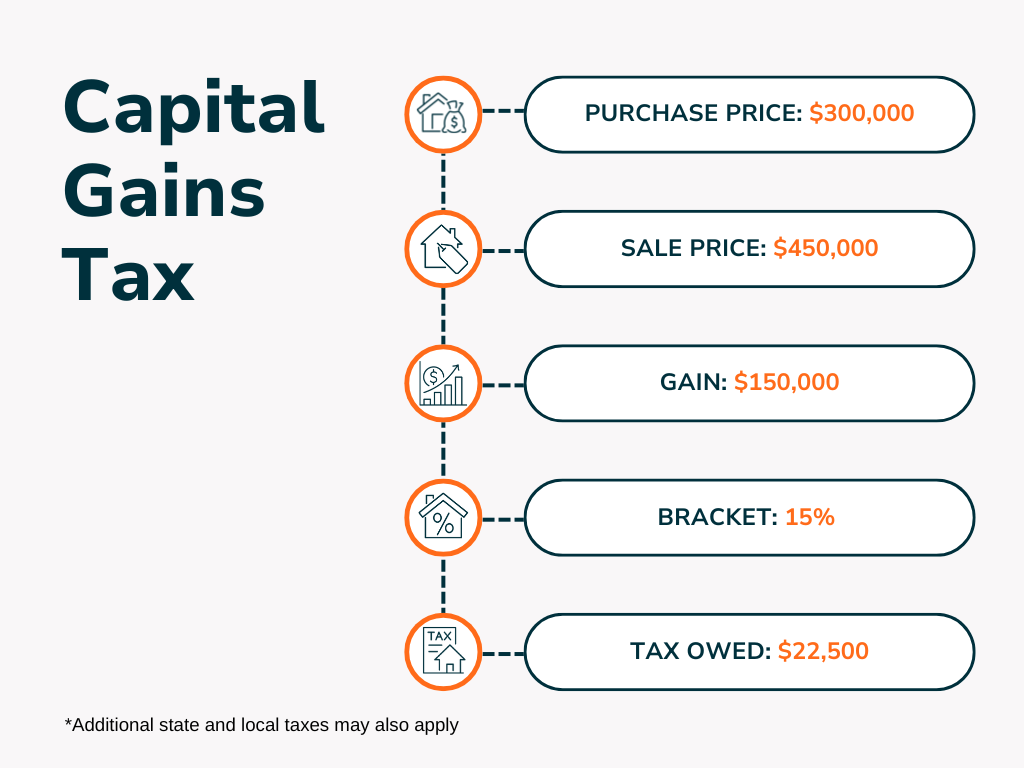

Imagine you bought an investment property for $300,000 and sold it five years later for $450,000. That’s a gain of $150,000. If you’re married, filing jointly, and your combined income is around $100,000, you’d likely fall into the 15% long-term capital gains bracket. That means you may owe capital gains tax of around $22,500—a number worth planning for.

The IRS does give you some levers to pull. Your primary residence may qualify for big exclusions. Investment properties have their own tax rules. Even details like closing costs and home improvements can reduce the size of your taxable capital gain. The trick is knowing which rules apply to you and how to use them to your advantage.

Understanding these basics is the first step to smart tax planning. From there, it’s about tailoring your strategies, whether that’s taking advantage of the primary residence exclusion, exploring a 1031 exchange, or making sure you're tracking every eligible expense.

Domain Money offers personalized, flat-fee financial planning with CFP® professionals who can help you minimize your capital gains tax on real estate through strategies that suit you and your finances. Our advisors will analyze your entire financial picture to help find the best approach for your situation.

Because this isn’t about finding a one-size-fits-all shortcut. You need to find the mix of strategies that match your goals, your property type, and your overall goals.

There are a number of smart, IRS-approved strategies that can help you keep more of your money working for you. Which one makes sense depends on your situation, goals, and timing.

Let’s break down the most effective approaches (promise we'll make it simple).

If you’ve owned and lived in your main home for at least two of the last five years, you may qualify for one of the best tax breaks available: the §121 home-sale exclusion.

Think of this as a homeowner’s “get-out-of-tax” card, but one you can only use once every two years.

For investors, a 1031 exchange is a powerful way to help keep your gains compounding.

Loads of investors use this repeatedly to build larger portfolios over time. But if you need some advice here, Domain Money is where you're going to find unbiased, fiduciary guidance with no asset-based fees. Our advisors are here to help you navigate all the complex requirements and timing involved in a 1031 exchange.

Rather than getting all your money at once, you can spread payments (and taxes) out with an installment sale.

Risk check: If the buyer defaults, you may need to foreclose. Careful contracts are essential here.

Your “cost basis” is what you paid for the property, but it’s not just the purchase price. Boosting your basis reduces the taxable gain.

Keep receipts and records. That $10,000 bathroom upgrade from a decade ago can still lower your tax bill today.

Also known as tax-loss harvesting, this strategy lets you balance real estate gains with losses from other investments like stocks or bonds.

If you’re already planning to give, donating appreciated property can deliver double benefits: a charitable deduction plus avoiding capital gains tax. Some investors even use charitable remainder trusts to keep receiving income while still reducing their tax burden.

Domain Money’s advisors can help you figure out the best approach for your situation—whether it’s structuring donations, setting up a charitable trust, or timing gifts strategically—so you can support causes you care about while keeping more of your wealth working for you.

There’s no one-size-fits-all answer. The right mix of strategies depends on your property, your timing, and your bigger financial goals. Whether you’re eyeing a move, upgrading your portfolio, or passing wealth to the next generation, smart tax planning can help you keep more of what you’ve earned.

Think of these strategies as tools in a toolbox. The real advantage comes from knowing which one (or combination) to use at the right time.

Selling real estate doesn’t end at the closing table. The IRS needs to hear about it, too. Reporting your sale properly isn’t just about avoiding penalties. It’s also about making sure you get credit for every tax break you qualify for.

Here’s what you need to know (and which forms to keep an eye on).

Most real estate sales show up on Schedule D and Form 8949. These forms record the nuts and bolts:

If you can exclude the entire gain under §121 and you did not receive a Form 1099-S, you generally don’t need to report the sale. Otherwise, you’ll need to complete Form 8949 and Schedule D.

In most cases, your closing agent files Form 1099-S to report your sale proceeds to both you and the IRS. You should receive your copy by January 31 of the year after the sale.

Pro tip: Don’t wait for that form to land in your mailbox. Start organizing your records (closing statements, receipts for improvements, proof of residency) as soon as the deal closes.

If you’re selling your main home and qualify for the full primary residence exclusion, you may not receive a 1099-S if you provide an acceptable written certification to the closing agent that the sale qualifies for the full exclusion.

But don’t skip the recordkeeping. Keep documents that prove you lived there for two of the past five years (utility bills, mortgage statements, or lease records can all help).

Doing a 1031 exchange? You’ll also need Form 8824, which details the like-kind exchange. While your qualified intermediary provides much of the info, the IRS holds you responsible for accurate reporting—so double-check everything.

If you’ll owe more than $1,000 in taxes and your regular withholding won’t cover it, the IRS expects quarterly estimated payments. Missing them can trigger penalties, even if you pay the full amount when you file your return. Think of it like paying your phone bill — late payments add unnecessary fees.

Hold onto all related documents for at least three years after filing. If you’re deferring gains with a 1031 exchange or installment sale, keep them even longer. Useful records include:

A well-organized paper trail protects you if questions ever come up down the line.

Even savvy property owners can trip up on tax rules. Here are the pitfalls to watch for, and how to sidestep them:

Bottom line: A little planning goes a long way. Know the rules, track your records, and don’t rush the process.

Real estate taxes can be tricky, and the stakes are high. Sometimes, the smartest money move isn’t doing it alone but knowing when to bring in backup.

Here are situations where a tax professional or financial planner can save you stress (and potentially money):

Selling real estate doesn’t have to mean losing a big chunk of your profits to capital gains tax. Understanding your options—from the primary residence exclusion to 1031 exchanges—and planning ahead can make a real difference. Keeping detailed records of improvements, knowing the timing rules, and calculating your cost basis accurately can genuinely help you save thousands, whether you’re selling a family home or an investment property.

But complex situations (and even the simpler ones) often benefit from some professional guidance. Tax laws change, and the strategies that worked last year might not apply today. Domain Money’s flat-fee CFP® professionals can help you navigate the rules, choose the right strategies for your circumstances, and create a plan that keeps more of your money working for you.

By planning ahead, keeping records, and seeking expert help when needed, you can minimize capital gains tax, protect your profits, and build long-term wealth. Connect with a Domain Money CFP® professional today and start your tailored tax strategy.

One common strategy is reinvesting the proceeds from a sold investment property through a 1031 exchange. You must identify the new property within 45 days and close within 180 days to defer capital gains tax.

The stepped-up basis is a tax provision that can benefit heirs. When someone inherits a property, its value is adjusted to the market price at the date of the death of the decedent. This can reduce or even eliminate capital gains taxes if the property is sold soon after.

Yes — if you’ve lived in the home as your main residence for at least two of the last five years, you may qualify for the Section 121 exclusion. This allows you to exclude up to $250,000 of gain if single, or $500,000 if married filing jointly, from your taxable income.

If you move out of your primary residence and rent it, the 6-year rule may let you claim the capital gains exclusion for up to six years under certain conditions. This can be a useful strategy if you’re temporarily relocating but want to preserve your tax benefits.