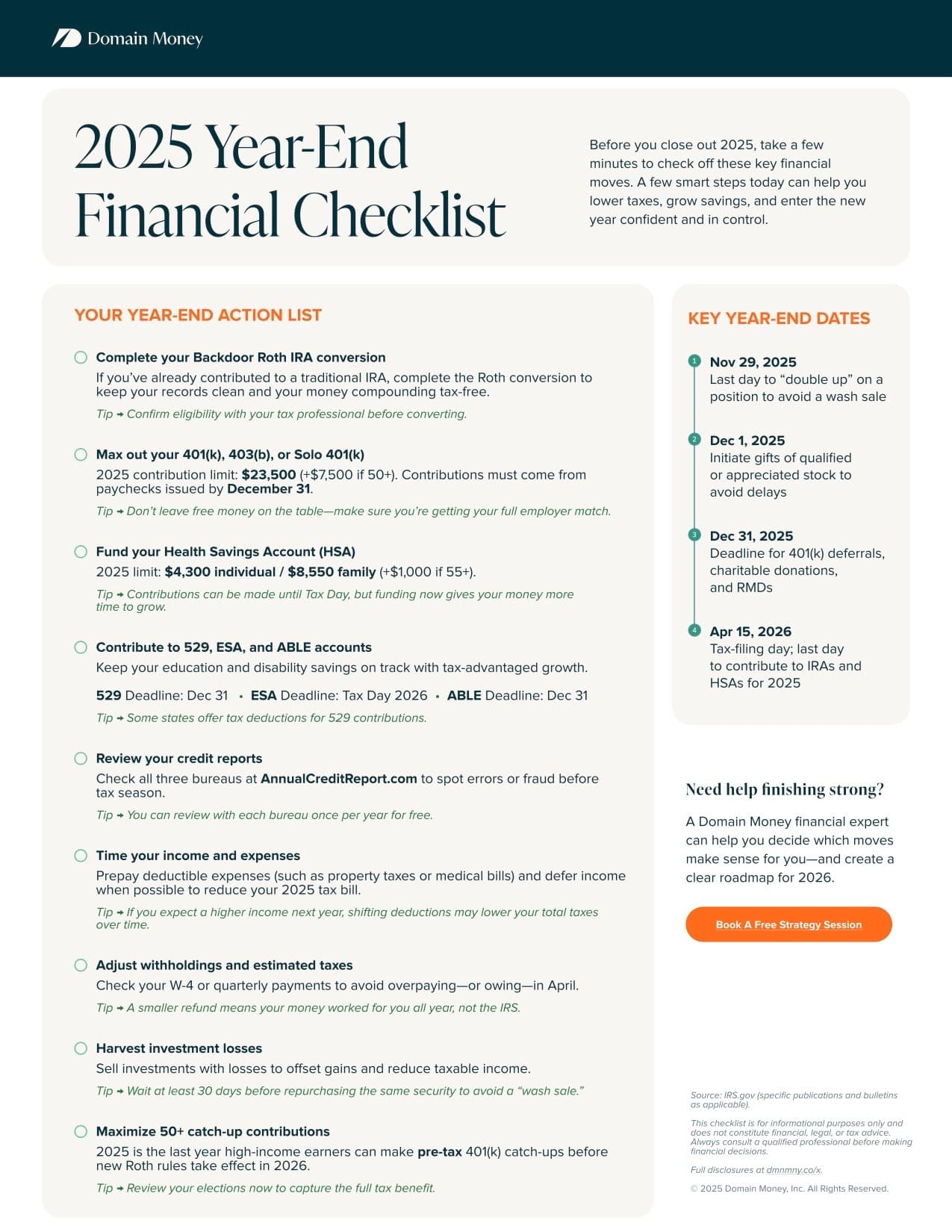

.jpg)

Last updated December 2025

You're earning $250,000. Your colleague earns $120,000. Yet somehow, they're building wealth faster than you are.

This paradox affects high earners across tech, finance, and consulting: despite substantial incomes, many professionals aren't accumulating net worth at the rate their earnings suggest they should.

Research shows that households earning $200,000-$250,000 have an average net worth of just $630,000. For context, at a 25% savings rate, someone earning $225,000 for just 10 years should have approximately $900,000 in assets (assuming 7% returns). The gap between what's possible and what's typical reveals a systematic problem with how high earners approach budgeting.

This guide addresses that gap. But unlike extreme approaches that demand lifestyle sacrifice, our framework focuses on strategic allocation—funding both the experiences that make life enjoyable and the wealth-building that creates long-term freedom.

Why Most Budgeting Advice Falls Short for Today's Professionals

Traditional budgeting advice assumes simple, predictable income streams and basic financial goals. But today's professionals—especially those in tech, finance, and consulting—face complex compensation structures that make standard budgeting frameworks inadequate.

Consider the challenges facing a typical high-earning professional:

- Irregular income from bonuses, RSUs, and stock options

- Progressive tax brackets claiming 32-37% of marginal income

- Multiple financial goals requiring sophisticated prioritization

- Lifestyle inflation pressure that can derail long-term wealth building

- Limited time for financial management despite high stakes

Research shows that professionals earning $200,000+ often feel as financially stressed as those earning half that amount. The culprit isn't insufficient income, but the lack of strategic frameworks designed for complex financial lives.

From Income Focus to Net Worth Focus

Before diving into tactical budgeting, high earners need a fundamental reframe: your income is a tool, your net worth is the goal.

Many professionals treat their increasing income as validation to expand spending proportionally. A $50,000 raise becomes a nicer apartment, a better car, more expensive vacations—all justifiable luxuries that nonetheless prevent wealth accumulation.

The net worth lens changes the question. Instead of "Can I afford this?" you ask "Does this purchase align with my net worth targets?"

Consider two approaches to a $50,000 raise:

Income-focused thinking: "I can now afford a $2,000/month apartment upgrade and a $70,000 car."

Net worth-focused thinking: "This raise can add $37,500 annually to investments (after taxes). Compounded over 15 years, that's $1.1 million in additional wealth. Is the apartment upgrade worth delaying financial independence by 3 years?"

Both approaches can be valid—the difference is making an explicit choice rather than defaulting to lifestyle expansion.

This doesn't mean rejecting enjoyment. It means designing a budget that intentionally funds experiences and lifestyle within a framework that prioritizes wealth velocity. At Domain Money, we want to work towards both goals simultaneously: a great life now, and financial freedom sooner.

The Complete Step-by-Step Budgeting Framework

Step 1: Calculate Your True Take-Home Pay

Most people dramatically overestimate their spendable income by focusing on gross rather than net pay. For high earners, this miscalculation can be catastrophic.

Calculate your monthly net income by starting with gross pay and subtracting:

- Federal income taxes (22-37% depending on bracket)

- State income taxes (0-13.3% by location)

- FICA taxes (7.65% on wages up to limits)

- Health insurance premiums

- 401(k) contributions

- HSA contributions

- Other pre-tax deductions

Example: A $150,000 salary in California becomes approximately $8,200 monthly take-home after taxes and standard deductions—not the $12,500 gross monthly income might suggest.

For professionals with equity compensation, calculate take-home pay separately for base salary (predictable) and variable income (bonuses, RSUs, options). This distinction becomes crucial for sustainable budgeting.

Step 2: Track Current Spending Patterns

Before creating budget categories, understand where your money actually goes. Many high earners discover they're unconsciously spending thousands monthly on convenience services, subscriptions, and lifestyle inflation.

Comprehensive tracking methods:

- Bank/credit card analysis: Review 3 months of statements categorizing every transaction

- App-based tracking: Use tools like Monarch Money, YNAB, or Personal Capital for automated categorization

- Expense receipt documentation: Photograph receipts for cash transactions and irregular expenses

- Monthly spending audits: Schedule 30-minute reviews to identify patterns and opportunities

Pay special attention to "subscription creep"—recurring charges that accumulate over time. High earners often discover $500+ monthly in forgotten subscriptions, premium services, and auto-renewals that provide minimal value.

Step 3: Implement Strategic Budget Allocation

The traditional 50/30/20 rule serves as a starting point, but high earners need modified allocations that optimize for wealth building and tax efficiency.

Modified allocation framework for high earners:

- 45-50% Fixed Necessities: Housing, utilities, insurance, groceries, transportation, childcare

- 15-20% Discretionary Spending: Entertainment, dining out, hobbies, personal care

- 30-35% Savings & Investments: Emergency fund, retirement accounts, goal-specific savings, tax planning

Priority order for the savings allocation:

- Emergency fund to 3-6 months expenses (12 months for high earners)

- Employer 401(k) match (free money up to match limit)

- Max 401(k) contributions ($24,500 for 2026, plus $8,000 catch-up if 50+)

- HSA maximum if eligible ($4,400 individual, $8,750 family for 2026)

- IRA contributions ($7,500 for 2026, or backdoor Roth if over income limits)

- Taxable investment accounts for additional wealth building

- Goal-specific savings (house down payment, education, major purchases)

Step 4: Automate Your Financial Success

Automation removes willpower from the wealth-building equation and ensures consistency regardless of busy schedules or market emotions.

Complete automation checklist:

- Paycheck splitting: Direct deposit percentages to checking (expenses), savings (emergency fund), and investment accounts

- Bill payment automation: Set up autopay for all fixed expenses to avoid late fees and decision fatigue

- Investment contributions: Automatic transfers to retirement and taxable investment accounts on paydays

- Savings increases: Schedule annual automation increases tied to raise percentages or bonus timing

Advanced automation for high earners:

- Tax withholding optimization: Adjust W-4 withholdings to account for equity compensation tax obligations

- Estimated quarterly payments: Automate payments for high earners who owe additional taxes beyond withholding

- Rebalancing schedules: Set calendar reminders for portfolio rebalancing and strategy reviews

Advanced Strategies for High-Income Professionals

Managing Equity Compensation Within Your Budget

Stock options, RSUs, and ESPP contributions require specialized budgeting approaches that traditional frameworks ignore.

RSU (Restricted Stock Unit) budgeting strategy:

- Budget based on base salary only—never incorporate unvested equity into living expenses

- Set aside 35-45% of RSU value upon vesting for tax obligations

- Implement systematic selling to avoid concentration risk exceeding 10% of net worth

- Use RSU income exclusively for wealth building, not lifestyle funding

Stock option optimization:

- Map exercise windows and expiration dates on annual calendar

- Calculate Alternative Minimum Tax implications for ISO exercises

- Coordinate option exercises with tax-loss harvesting opportunities

- Consider financing strategies for large option exercises

Tax-Efficient Budgeting for High Brackets

High earners face marginal tax rates of 32-37% federal plus state taxes, making tax efficiency crucial to effective budgeting.

Key tax optimization strategies:

- Maximize pre-tax contributions: Every dollar in 401(k)/HSA saves 32-50% in combined taxes

- Time income recognition: Defer bonuses to lower-tax years when possible

- Coordinate charitable giving: Bunch deductions every other year to exceed standard deduction

- Geographic arbitrage: Consider state tax implications for remote work opportunities

Tax withholding management for variable income:High earners with bonuses or equity compensation often face large tax bills because standard withholding assumes consistent income throughout the year. Consider increasing W-4 withholding or making quarterly estimated payments to avoid underpayment penalties.

Common Budgeting Mistakes High Earners Must Avoid

Lifestyle Inflation Trap

The biggest wealth-building killer isn't market crashes or bad investments—it's the gradual increase in spending that absorbs income growth.

Warning signs of dangerous lifestyle inflation:

- Budget creep without conscious decisions about increased spending

- Feeling financially stressed despite substantial income increases

- Inability to increase savings rates even as income grows

- Justifying premium purchases as "investments" or "necessities"

Prevention strategies:

- Implement the "50% rule": half of any raise goes to increased savings

- Conduct quarterly lifestyle audits to identify unconscious spending increases

- Set concrete spending limits for discretionary categories with automatic enforcement

- Focus on "values-based spending" that aligns with long-term goals

Inadequate Emergency Fund for Income Complexity

High earners often underestimate emergency fund needs because their income provides a false sense of security.

Why high earners need larger emergency funds:

- Job replacement difficulty: Only 2% of positions pay $250,000+

- Industry volatility: Tech, finance, and consulting face periodic layoffs

- Lifestyle complexity: Higher fixed costs that can't be quickly reduced

- Career transition timing: Senior roles require longer job search periods

Target 12 months of necessity expenses (not total spending) for high earners, focusing on mortgage/rent, utilities, groceries, transportation, childcare, and insurance premiums.

Real-World Budgeting Scenarios

Scenario 1: Tech Professional with Variable Compensation

Profile: Senior Product Manager, $180,000 base + $120,000 annual RSUs

Challenge: Managing irregular equity income while building wealth efficiently

Strategic approach:

- Budget all fixed expenses and lifestyle on base salary only ($180,000)

- Treat RSU income as pure wealth building opportunity

- Set aside 40% of RSU proceeds for taxes immediately upon vesting

- Automate remaining RSU proceeds to diversified investment accounts

- Maintain 15-month emergency fund due to tech industry volatility

Results: Sustainable lifestyle independent of company performance, accelerated wealth building through systematic equity diversification, tax efficiency through proactive planning.

Scenario 2: Dual-Income Professional Couple

Profile: Management consultants earning $160,000 and $140,000 ($300,000 combined)

Challenge: Coordinating complex travel schedules, irregular hours, and planning for family expansion

Strategic framework:

- Budget based on lower earner's income ($140,000) for all fixed expenses

- Higher earner's income funds savings goals and discretionary spending

- Separate "travel and convenience" budget category for work-related lifestyle needs

- Joint investment accounts with individual discretionary spending accounts

- Automatic savings rate increases tied to performance bonuses

Results: Financial flexibility for career transitions, family planning, or geographic moves while maintaining aggressive wealth building.

When to Seek Professional Financial Planning Help

DIY budgeting works well for straightforward financial situations, but high earners often reach complexity thresholds where professional guidance provides substantial value.

Consider CFP® professional guidance when you have:

- Equity compensation requiring tax optimization

- Multi-state tax complications

- Estate planning needs beyond basic wills

- Charitable giving strategies

- Business ownership or 1099 income

- Complex insurance needs (disability, umbrella, life)

- Investment portfolios exceeding $500,000

Evaluate advisor fee structures carefully: A 1% AUM fee on a $1 million portfolio costs $10,000 annually—money that compounds to $266,000 over 20 years. Flat-fee financial planning often provides better value alignment for high earners focused on comprehensive planning rather than just investment management.

Domain Money's approach eliminates the conflicts inherent in percentage-based fees, providing transparent annual pricing that scales with service complexity rather than asset levels. This alignment ensures recommendations focus on your financial success rather than maximizing advisor compensation.

Frequently Asked Questions

What percentage of income should I save if I earn over $200,000?

High earners should target 25-35% savings rates, significantly higher than the standard 20% recommendation. This accounts for progressive tax impacts, income replacement challenges, and accelerated wealth-building opportunities. Prioritize maxing out tax-advantaged accounts first ($24,500 401k + $7,500 IRA + $4,400+ HSA for 2026), then add taxable investments. The key is automating savings increases with income growth to prevent lifestyle inflation from absorbing raises and bonuses.

How do I budget when my income varies significantly month to month?

Create separate budgets for base income and variable income. Cover all living expenses and fixed savings goals with your predictable base income only. Treat bonuses, commissions, or equity compensation as "wealth acceleration" money that goes directly to emergency funds, debt payoff, or additional investments. This approach provides lifestyle stability regardless of income volatility while maximizing wealth building during high-earning periods.

Should I pay off debt or invest when I have extra money?

Focus on eliminating high-interest debt (credit cards, personal loans) first, as guaranteed savings of 15-25% interest rates typically exceed investment returns. For lower-interest debt like mortgages, consider your tax bracket—high earners receive substantial tax benefits from mortgage interest deductions. A 4% mortgage effectively costs 2.5-3% after taxes in high brackets, making investment returns potentially more attractive than accelerated payoff.

How large should my emergency fund be as a high earner?

High earners need 12 months of necessity expenses, not the standard 3-6 months. Calculate based on mortgage/rent, utilities, groceries, transportation, childcare, and insurance premiums—exclude discretionary spending. The rationale: replacing $200,000+ income takes significantly longer than replacing average salaries, and high earners often have higher fixed costs that can't be quickly reduced during unemployment.

Is the 50/30/20 budget rule still relevant for high-income earners?

The 50/30/20 rule needs modification for high earners. Use 45-50% for necessities, 15-20% for discretionary spending, and 30-35% for savings and investments. High earners face different challenges: progressive tax brackets, complex compensation, and greater wealth-building opportunities that require higher savings rates. Focus on maximizing tax-advantaged accounts before calculating discretionary spending, and automate savings increases to prevent lifestyle inflation.

Take Control of Your Financial Future Today

Effective budgeting transforms from expense management into strategic wealth building when implemented with frameworks designed for your income complexity. The difference between financial stress and financial confidence often comes down to having systems that automate good decisions and prevent common high-earner pitfalls.

Your next steps:

- Calculate your true take-home pay including all taxes and deductions

- Implement modified budget allocations with 30-35% savings targets

- Automate your savings and investment contributions to remove willpower from wealth building

- Set up separate treatment for base salary (lifestyle) and variable income (wealth building)

- Schedule quarterly budget reviews to optimize and adjust as income grows

Ready to optimize your financial strategy? Domain Money's flat-fee CFP® professionals specialize in helping high earners maximize their wealth-building potential through comprehensive planning that goes far beyond basic budgeting.

Our transparent fee structure eliminates the conflicts present in AUM-based advice, ensuring our recommendations focus on your financial success rather than maximizing our compensation. Whether you're navigating equity compensation, optimizing tax strategies, or coordinating complex financial goals, we provide the expertise and accountability that transforms good intentions into lasting wealth.

Book your free strategy session to discover how strategic financial planning can accelerate your path to financial independence while providing confidence in every financial decision.

Domain Money is rated 4.7/5 stars on Trustpilot based on hundreds of client reviews.

Disclaimer: This information is for educational purposes only and should not be considered personalized financial advice. Every financial situation is unique, and strategies should be tailored to individual circumstances, goals, and risk tolerance. Please consult with a qualified CFP® professional before making significant financial decisions. Domain Money provides comprehensive financial planning services to help clients achieve their goals through transparent, fee-only advice.

.png)

.jpeg)